AUGUST 1, 2026

Silver Slide Puts Metals Market on Fed Watch as US Dollar Reasserts PressureSilver stays under pressure as traders weigh Federal Reserve signals, US Dollar strength and industrial demand in the metals market.

© 1box.site 2026

JULY 11, 2026

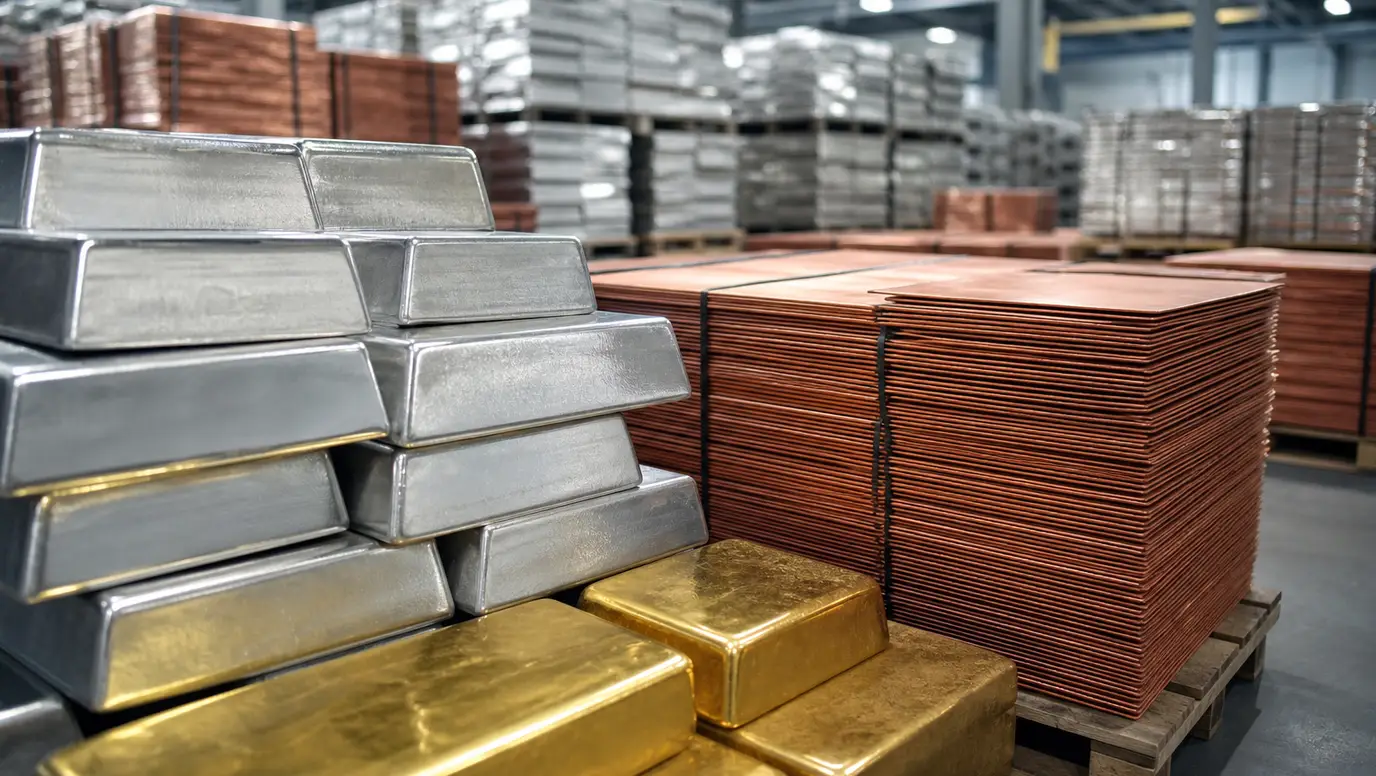

The metals market entered the weekend with copper drawing the strongest fresh attention, as traders focused less on a simple direction call and more on the widening policy premium embedded in US pricing. Early Saturday indications showed COMEX copper holding near $6.28 a pound, while gold hovered around $4,129 an ounce and silver traded near $60.30 an ounce. The split leaves copper as the clearest stress point in the complex, even as precious metals remain sensitive to the US dollar, Treasury yields and Federal Reserve expectations.

The latest move is not just about industrial demand. Copper is being pulled between physical tightness, inventory relocation and uncertainty over whether US import policy will extend more directly into refined metal. That possibility has kept the US market better supported than global benchmarks and has made the COMEX premium a key gauge for manufacturers, fabricators and speculative funds trying to price supply-chain risk before any policy clarity arrives.

For investors, the story is increasingly about market structure. A copper price that rises because end demand is improving sends one signal; a copper price that rises because metal is being diverted toward the United States ahead of potential tariffs sends another. The first implies a broad-cycle growth impulse. The second can create regional shortages, temporary dislocations and abrupt reversals if policy risk is resolved differently than traders expect.

Copper’s strength has been reinforced by the perception that US buyers may need to secure material before policy changes affect import costs. That has encouraged a continued focus on exchange inventories and regional spreads rather than on headline spot prices alone. The buildup of metal in US-registered warehouses over recent months has eased some near-term delivery concerns, but it has also highlighted how aggressively trade flows have shifted in response to tariff expectations.

The result is a market where the same metal can tell different stories depending on the venue. US futures continue to reflect a premium for domestic availability, while global prices remain more exposed to China’s mixed macro signals and to questions about whether high copper prices will eventually curb demand from manufacturers. This is why traders are watching not only whether copper holds above recent support, but whether the premium between US and international pricing narrows or widens into the next policy window.

Underlying demand remains a supportive counterweight. Electrification, grid upgrades, data-center power needs and electric-vehicle supply chains continue to strengthen copper’s medium-term investment case. At the same time, the old-economy side of demand remains uneven, particularly where property, construction and traditional manufacturing are not yet showing a synchronized recovery. That tension has made copper one of the most news-sensitive metals in the current commodity landscape.

Gold and silver are not leading the latest metals narrative, but they remain important because their reaction to macro data can either validate or challenge the copper move. Gold’s failure to build a more decisive advance above the $4,200 area earlier this week showed that safe-haven demand is still competing with a stubborn rate backdrop. When Treasury yields rise or the US dollar firms, non-yielding metals tend to lose part of their appeal, even when geopolitical risk remains present.

Silver has been more volatile. Its industrial profile gives it some connection to copper’s demand story, but its investment profile keeps it tied to gold and real-rate expectations. That dual identity has left silver vulnerable to sharper intraday swings whenever traders reassess the path of Fed policy. A move back above recent resistance would improve sentiment, but a failure to hold the $60 area would likely invite more cautious positioning from momentum accounts.

The Federal Reserve remains central to the precious-metals outlook. Markets are still balancing signs of slower labor momentum against inflation concerns and a policy stance that has not turned clearly dovish. Until that balance shifts, gold may continue to trade as a high-level consolidation rather than a clean breakout, while silver may remain more exposed to liquidation risk when yields move higher.

The immediate metals-market checklist is unusually crowded. Copper traders are watching tariff headlines, exchange warehouse flows, US physical premiums and China demand indicators. Gold and silver traders are watching the US dollar, Treasury yields and the next inflation readings. Any combination of softer inflation and a weaker dollar could revive precious-metals buying, but a renewed rise in yields would likely cap rallies.

For copper, the more important question is whether the current premium reflects a durable re-pricing of supply risk or a temporary distortion created by policy uncertainty. If tariff fears intensify, US copper could stay firm even if global benchmarks struggle. If the policy risk fades, the market may have to reprice inventories that were pulled forward into the United States, potentially narrowing regional spreads and reducing the urgency behind recent buying.

That leaves the broader metals complex in a cautious but active setup. Copper is carrying the strongest current news impulse because it sits at the intersection of trade policy, physical logistics and long-term electrification demand. Gold and silver remain supported by macro uncertainty, but their upside is still being filtered through the rate market. Until one of those forces breaks decisively, the metals market is likely to remain selective, with copper premiums offering the clearest real-time signal of where stress is building.

AUGUST 1, 2026

Silver Slide Puts Metals Market on Fed Watch as US Dollar Reasserts Pressure

JULY 26, 2026

Gold and Silver Hold Firm as Metals Traders Brace for Federal Reserve Signal

JULY 20, 2026

Silver Leads Metals as Gold Stalls Near $4,000 on Oil-Driven Inflation Risk

JULY 19, 2026

Gold and Silver Enter Federal Reserve Week Under Pressure as US Dollar and Yields Bite

JULY 18, 2026

Copper Pullback Keeps Metals Market Defensive as Gold and Silver Watch Yields

JULY 16, 2026

Gold Holds Above $4,000 as Silver Slide Puts Metals Market on Federal Reserve Watch

JULY 14, 2026

Gold and Silver Jump as Cool CPI Pulls Metals Market Back Toward Real-Yield Trade

JULY 13, 2026

Silver Slides as Yield Shock Overpowers Haven Demand in Metals Market

JULY 10, 2026

Silver and Copper Rebound as Softer US Dollar Revives Metals Market Bid

JULY 7, 2026

Platinum and Palladium Buck Gold Slide as Asia Bullion Moves Reshape Metals Market

JULY 5, 2026

Copper Tariff Delay Keeps Metals Market on Edge as Gold Holds Jobs-Report Rebound

JULY 4, 2026

Silver and Zinc Lead Broad Metals Rally as Dollar Weakness Extends Holiday Bounce

JULY 2, 2026

Gold and Silver Regain Momentum as Softer Jobs Signals Pull Yields Lower

JUNE 30, 2026

Gold Nears Worst Quarter Since 2013 as Fed Bets Reprice Metals Market

JUNE 29, 2026

Silver Breaks Below $60 as Dollar Pressure Spills Into Copper