JULY 20, 2026

US Dollar Tests Japanese Yen Intervention Zone as Forex Market Prices Oil ShockUS dollar steadies near recent highs against the Japanese yen as oil-driven risk aversion reshapes forex positioning before central bank meetings.

© 1box.site 2026

JUNE 29, 2026

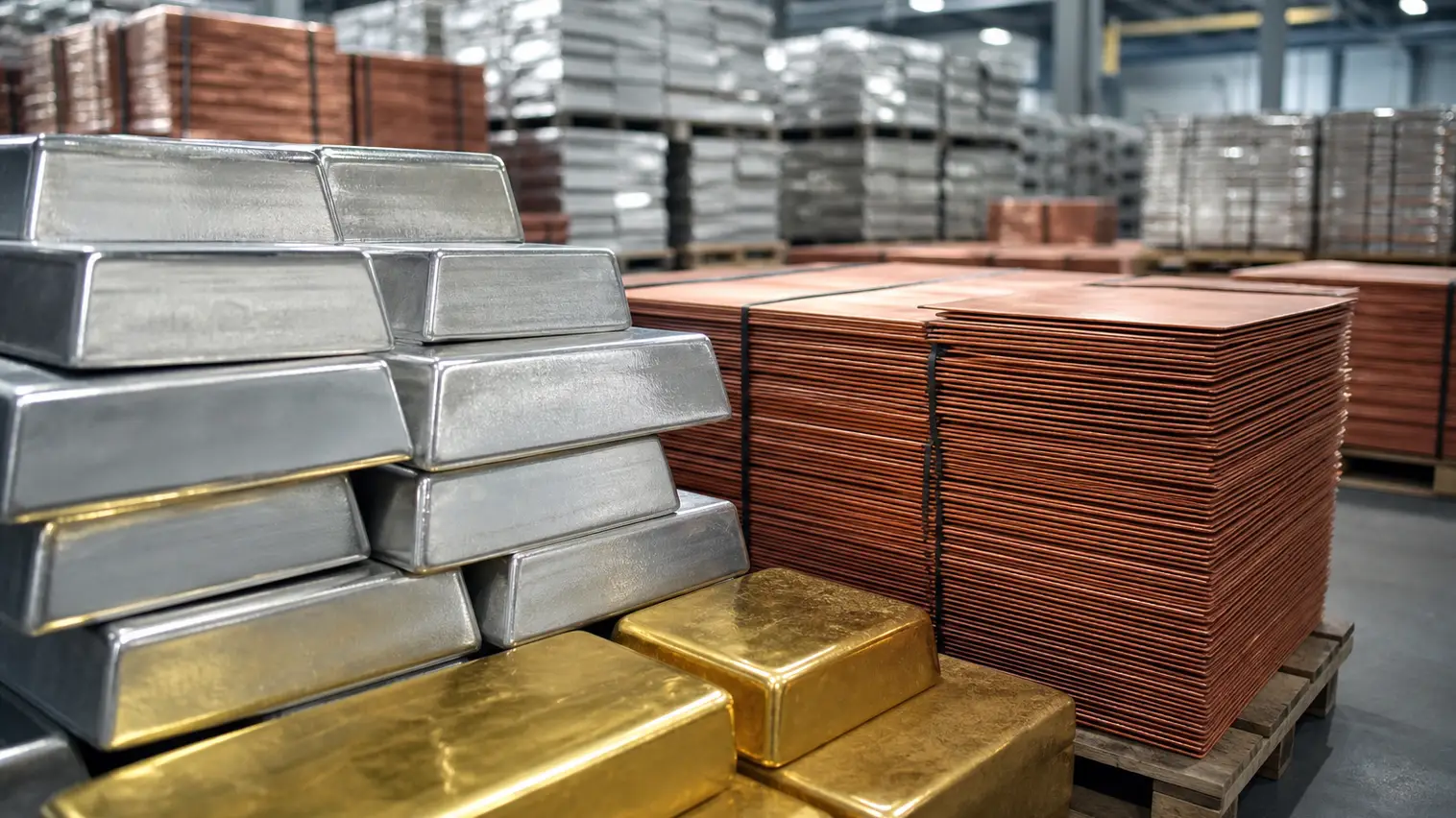

Silver led a renewed metals retreat on Monday as a firmer US Dollar and persistent Federal Reserve rate concerns pushed traders back into defensive positioning before the end of the quarter. The move kept pressure on precious metals while also spilling into copper, showing that the latest selloff is not limited to safe-haven demand but is affecting the broader metals complex.

Spot silver traded below the $60 area in early market activity, extending a sharp correction from the elevated levels seen earlier this year. Gold also struggled to hold its rebound, with traders reluctant to rebuild long exposure while real-yield expectations remain firm and the US Dollar stays supported by the market’s view that monetary policy may remain restrictive for longer.

The latest decline reflects a familiar pressure point for precious metals: higher expected interest rates reduce the appeal of non-yielding assets. Silver is especially vulnerable because it trades as both a monetary metal and an industrial input, leaving it exposed to shifts in Fed expectations as well as concerns about demand from manufacturing, electronics and solar supply chains.

The break below $60 does not by itself confirm a deeper trend reversal, but it has changed the short-term tone. Momentum traders are now watching whether silver can quickly reclaim lost ground or whether the market begins to price a wider liquidation phase across precious metals. Gold remains a key reference point, but silver’s sharper moves are setting the pace for metals sentiment.

Copper also moved lower as macro pressure reached base metals. The red metal had been supported earlier in June by supply concerns and trade-related positioning, but the stronger dollar and renewed caution on global growth have made it harder for buyers to defend recent gains. A softer copper tape suggests industrial metals are now absorbing the same financial-condition shock that has already hit gold and silver.

For investors, the important signal is the alignment between precious and base metals. When silver, gold and copper fall together, the market is usually responding less to metal-specific supply stories and more to broader liquidity, currency and interest-rate expectations. That makes upcoming US inflation readings, labor-market data and Fed commentary critical for the next directional move.

Quarter-end positioning could amplify price swings across the metals market. Funds that built exposure to precious metals during the earlier inflation-hedge rally may continue trimming risk if the dollar remains firm, while industrial-metal buyers may wait for clearer signals from China demand and US trade policy before adding fresh length.

Still, the selloff has not erased the longer-term themes supporting metals. Central-bank demand, constrained mine supply and electrification-linked consumption remain part of the broader backdrop. In the near term, however, the market is trading on policy risk first. Until yields ease or the dollar loses momentum, rallies in silver, gold and copper may be treated as corrective rather than decisive.

JULY 20, 2026

US Dollar Tests Japanese Yen Intervention Zone as Forex Market Prices Oil Shock

JULY 19, 2026

Gold and Silver Enter Federal Reserve Week Under Pressure as US Dollar and Yields Bite

JULY 19, 2026

Forex Market Faces Euro and Japanese Yen Test as US Dollar Meets Federal Reserve and ECB Week

JULY 18, 2026

US Dollar Finds Haven Bid as British Pound Gains and Japanese Yen Risk Test Forex Market

JULY 17, 2026

US Dollar Set for Weekly Loss as Euro Holds Ground and Japanese Yen Keeps Forex Market on Edge

JULY 17, 2026

Brent Crude and WTI Crude Hold Weekly Gains as Red Sea Threat Offsets US Dollar Rebound

JULY 16, 2026

Forex Market Braces for Retail Sales as US Dollar Slump Tests Japanese Yen and Federal Reserve Bets

JULY 16, 2026

LNG and Gas Prices Keep Energy Market on Edge as US Dollar Weakens

JULY 15, 2026

US Dollar Stays Defensive in Forex Market as Cooler PPI Lifts Euro and British Pound

JULY 14, 2026

Gold and Silver Jump as Cool CPI Pulls Metals Market Back Toward Real-Yield Trade

JULY 14, 2026

US Dollar Slides as Cool CPI Lifts Euro and Checks Yen Pressure

JULY 13, 2026

British Pound Slips as US Dollar Haven Bid Builds Before US CPI

JULY 13, 2026

Silver Slides as Yield Shock Overpowers Haven Demand in Metals Market

JULY 12, 2026

Canadian Dollar Rebound Puts USD/CAD on Alert Before Bank of Canada Decision

JULY 12, 2026

Gold Bulls Face Oil-Inflation Trap as Metals Market Watches $4,000 Support

JULY 11, 2026

Yen Rally Tests US Dollar Carry Trade as Japan Weighs Pension-Fund Pivot

JULY 10, 2026

Silver and Copper Rebound as Softer US Dollar Revives Metals Market Bid

JULY 10, 2026

US Dollar-Euro Standoff Turns to CPI as Central Bank Minutes Narrow Forex Breakout

JULY 9, 2026

US Dollar Firms as Oil Shock and Fed Minutes Push Yen Back Toward Lows

JULY 9, 2026

Brent Nears $79 as Renewed Gulf Risk Rebuilds Crude Oil Premium

JULY 8, 2026

Gold Loses Haven Bid as Dollar Strength Splits the Metals Market

JULY 8, 2026

New Zealand Dollar Rallies as RBNZ Rate Hike Reopens Forex Carry Trade

JULY 7, 2026

Platinum and Palladium Buck Gold Slide as Asia Bullion Moves Reshape Metals Market

JULY 7, 2026

Dollar Drift Keeps Forex Market on Fed Minutes Watch as Euro Softens and Yen Sinks

JULY 6, 2026

Japanese Yen Keeps Forex Market on Intervention Alert as Dollar Steadies Near Two-Week Low

JULY 6, 2026

Gold Pullback and Copper Resilience Split Metals Market as Dollar Stabilizes

JULY 5, 2026

Copper Tariff Delay Keeps Metals Market on Edge as Gold Holds Jobs-Report Rebound

JULY 5, 2026

Dollar Rebound Puts Forex Market on Fed Minutes Watch After Payroll Shock

JULY 4, 2026

Australian Dollar Leads FX Rebound as Weak US Jobs Data Tests 70-Cent Barrier

JULY 4, 2026

Silver and Zinc Lead Broad Metals Rally as Dollar Weakness Extends Holiday Bounce