JULY 20, 2026

US Dollar Tests Japanese Yen Intervention Zone as Forex Market Prices Oil ShockUS dollar steadies near recent highs against the Japanese yen as oil-driven risk aversion reshapes forex positioning before central bank meetings.

© 1box.site 2026

JUNE 28, 2026

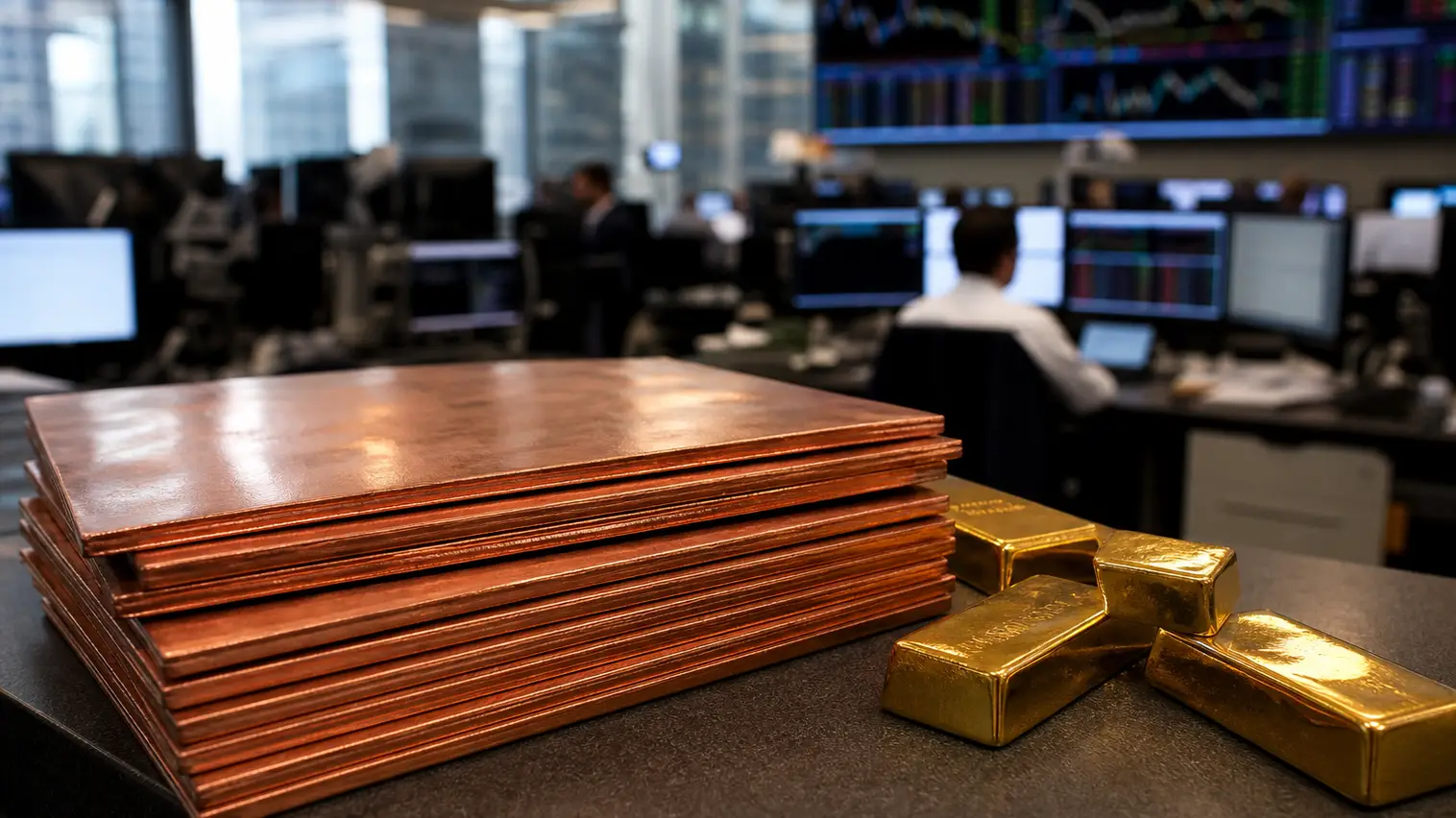

The metals market is entering the final sessions of June with copper back at the center of trading desks, as a looming U.S. tariff recommendation threatens to reshape physical flows just as precious metals attempt to stabilize from a volatile month. Weekend indications showed gold holding near the low $4,000s per ounce, silver close to $59 per ounce and COMEX copper around $6.20 per pound, leaving traders focused less on one directional move and more on which metal carries the clearest catalyst into quarter-end.

Fresh news activity is strongest in metals rather than foreign exchange because the sector now has two live themes moving at once: policy risk in copper and renewed haven demand in gold. Currency markets remain important through the U.S. dollar and Treasury yields, but the more immediate market tension is being expressed in metal spreads, warehouse positioning and procurement decisions ahead of the June 30 policy checkpoint.

Copper is drawing the heaviest attention because traders are watching whether Washington moves closer to tariffs on refined copper imports. The market has already spent much of the second quarter adjusting to the possibility of new duties, with U.S. inventories elevated after earlier stockpiling and the COMEX premium over London narrowing from more extreme levels. That shift suggests the most aggressive import scramble has cooled, but it does not remove the risk of a fresh repricing if the recommendation is stricter than expected.

For industrial buyers, the key issue is not only the headline tariff rate. A phased implementation, an exemption extension or a narrower product scope would each send a different signal to fabricators, cable producers and manufacturers planning third-quarter coverage. If the tariff threat fades, some of the metal parked in U.S. warehouses could become easier to release back into the market. If the threat hardens, domestic premiums may stay sticky even if global copper prices soften.

That makes copper a more policy-sensitive trade than a simple demand story this week. Structural demand from grids, electrification, data centers and industrial buildout remains a medium-term support, while mine disruptions and smelter feed constraints continue to limit confidence in supply growth. Near term, however, traders are likely to treat the tariff decision as the first test before returning to broader questions about Chinese demand, manufacturing activity and global inventories.

Gold’s rebound is also keeping the metals market active, though its driver is different. The metal has recovered from recent pressure as investors reassess whether higher U.S. yields and a firm dollar can continue to cap non-yielding assets. With spot prices still holding above the psychologically important $4,000 area, the market is signaling that strategic demand has not disappeared even after a sharp round of volatility.

Silver is trading with a more aggressive profile because it sits between precious-metal demand and industrial sensitivity. Its move back toward the upper-$50s per ounce region has improved sentiment, but it also raises the risk of faster profit-taking if the dollar strengthens or if copper loses momentum. Platinum and palladium remain secondary stories, supported by broader metals flows but still constrained by uneven expectations for automotive and industrial demand.

The dollar and Treasury yields remain the main macro variables for precious metals. A softer dollar would make gold and silver more attractive to non-U.S. buyers, while falling yields would reduce the opportunity cost of holding bullion. Conversely, any renewed rise in real yields could quickly turn the latest rebound into a consolidation phase rather than the start of a broader breakout.

Quarter-end positioning adds another layer of risk. Portfolio managers that reduced metals exposure during the recent pullback may be forced to reconsider allocations if copper holds firm and gold refuses to break down. At the same time, funds with strong first-half gains may prefer to lock in profits before fresh policy guidance and early-July macro data arrive.

The result is a metals market that looks less synchronized than it did earlier in the year. Copper is trading on tariffs, inventories and physical premiums. Gold is trading on rates, the dollar and haven demand. Silver is trying to follow both at once. That split could keep volatility elevated even if headline prices appear steady in thin weekend and quarter-end conditions.

For now, the strongest signal is that metals traders are no longer treating the sector as a single macro trade. Copper’s tariff deadline has created a distinct industrial catalyst, while gold’s resilience shows that defensive demand remains alive. If Washington delivers a clear copper roadmap and U.S. yields stay contained, the metals market could begin July with a firmer tone. If the policy message is ambiguous and the dollar rebounds, the next move may be defined by wider spreads rather than broad-based gains.

JULY 20, 2026

US Dollar Tests Japanese Yen Intervention Zone as Forex Market Prices Oil Shock

JULY 19, 2026

Gold and Silver Enter Federal Reserve Week Under Pressure as US Dollar and Yields Bite

JULY 19, 2026

Forex Market Faces Euro and Japanese Yen Test as US Dollar Meets Federal Reserve and ECB Week

JULY 18, 2026

US Dollar Finds Haven Bid as British Pound Gains and Japanese Yen Risk Test Forex Market

JULY 17, 2026

US Dollar Set for Weekly Loss as Euro Holds Ground and Japanese Yen Keeps Forex Market on Edge

JULY 17, 2026

Brent Crude and WTI Crude Hold Weekly Gains as Red Sea Threat Offsets US Dollar Rebound

JULY 16, 2026

Forex Market Braces for Retail Sales as US Dollar Slump Tests Japanese Yen and Federal Reserve Bets

JULY 16, 2026

LNG and Gas Prices Keep Energy Market on Edge as US Dollar Weakens

JULY 15, 2026

US Dollar Stays Defensive in Forex Market as Cooler PPI Lifts Euro and British Pound

JULY 14, 2026

Gold and Silver Jump as Cool CPI Pulls Metals Market Back Toward Real-Yield Trade

JULY 14, 2026

US Dollar Slides as Cool CPI Lifts Euro and Checks Yen Pressure

JULY 13, 2026

British Pound Slips as US Dollar Haven Bid Builds Before US CPI

JULY 13, 2026

Silver Slides as Yield Shock Overpowers Haven Demand in Metals Market

JULY 12, 2026

Canadian Dollar Rebound Puts USD/CAD on Alert Before Bank of Canada Decision

JULY 12, 2026

Gold Bulls Face Oil-Inflation Trap as Metals Market Watches $4,000 Support

JULY 11, 2026

Yen Rally Tests US Dollar Carry Trade as Japan Weighs Pension-Fund Pivot

JULY 10, 2026

Silver and Copper Rebound as Softer US Dollar Revives Metals Market Bid

JULY 10, 2026

US Dollar-Euro Standoff Turns to CPI as Central Bank Minutes Narrow Forex Breakout

JULY 9, 2026

US Dollar Firms as Oil Shock and Fed Minutes Push Yen Back Toward Lows

JULY 9, 2026

Brent Nears $79 as Renewed Gulf Risk Rebuilds Crude Oil Premium

JULY 8, 2026

Gold Loses Haven Bid as Dollar Strength Splits the Metals Market

JULY 8, 2026

New Zealand Dollar Rallies as RBNZ Rate Hike Reopens Forex Carry Trade

JULY 7, 2026

Platinum and Palladium Buck Gold Slide as Asia Bullion Moves Reshape Metals Market

JULY 7, 2026

Dollar Drift Keeps Forex Market on Fed Minutes Watch as Euro Softens and Yen Sinks

JULY 6, 2026

Japanese Yen Keeps Forex Market on Intervention Alert as Dollar Steadies Near Two-Week Low

JULY 6, 2026

Gold Pullback and Copper Resilience Split Metals Market as Dollar Stabilizes

JULY 5, 2026

Copper Tariff Delay Keeps Metals Market on Edge as Gold Holds Jobs-Report Rebound

JULY 5, 2026

Dollar Rebound Puts Forex Market on Fed Minutes Watch After Payroll Shock

JULY 4, 2026

Australian Dollar Leads FX Rebound as Weak US Jobs Data Tests 70-Cent Barrier

JULY 4, 2026

Silver and Zinc Lead Broad Metals Rally as Dollar Weakness Extends Holiday Bounce